If you are a privilege or private banking client with a bank, you should have been broached with the idea of purchasing a structured note, or an Equity-Linked Note (ELN) with the cash savings you have. On the surface, it sounds really attractive, but what exactly is this instrument about and why do you need to be careful?

How does an Equity-Linked Note (ELN) work?

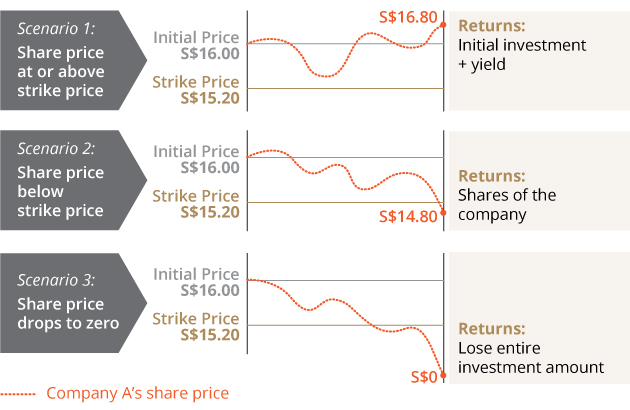

There are several different variations, but most of them bear the same semblance. For simplicity, we will look at the ELN comprising of only 1 stock (e.g. Alibaba). Next they will decide with you what is the principal amount you want to invest. Say $100k, and they will give you a small discount so that you only need to put in $99k for example. But at the maturity, if things go well, you will get back $100k. On top of that, they promise a certain high-yield coupon payout every month or every quarter if things go well. By now, you will notice the term ‘if things go well’ as a disclaimer. Next, they will determine the spot price for each of your stocks, which is usually the current market price of the stocks. Then there will be a strike price set for each individual stock, which means that if the close price falls below this strike price, you will be forced to buy the underlying stocks at that lower price. So for example, if Alibaba is the stock chosen and the spot price was set at $180 and strike price at $150. So if the markets drop, and Alibaba stock drops to $140, you will need to buy $100k/$150 = 666.6 units of Alibaba stock at $150 each. But if the closing price is above the strike price, the client will get the promised coupon and $100k at the maturity.

So why is this a bad deal?

Obviously, this deal works out alright if markets are doing well and Alibaba stock climbs or doesn’t fall too badly. The client will enjoy the promised coupons and the final principal amount. But if the client is already optimistic about the markets, why not just go directly and buy the Alibaba stock itself? Why markets are going up, client will still enjoy the full gains of the stock price. But nevertheless, if client’s prediction of Alibaba stock price is positive, everyone is happy.

But what happens if Alibaba stock falls?

If the stock falls but not too much such that it is still above the strike price, client still enjoys the coupons and the principal amount. So that is some margin of safety for the client. But what if Alibaba stock falls significantly? The client will be forced to buy Alibaba stock at the strike price, which is above the current market price of Alibaba stock, which means the client will be buying the stock at a more expensive price than what the markets are valuing it now. In a nutshell, client almost bears all the risk. If things go well, they enjoy the promised returns, but if things go south, client is stuck holding on to stocks that have depreciated in value.

So why do banks offer this?

Essentially, banks are using clients to fund the sales of their put-options to other clients. Writing options is another way banks make money. Put-options are basically contracts they sell to customers, which gives the customer a right to sell a certain stock at a certain price to the bank. So for example, if a customer owns Alibaba stocks, but he is fearful that Alibaba stock might crash. So he might choose to buy a put-option from a bank that allows him to sell his Alibaba stocks to the bank at a certain price at a certain date. So even if Alibaba stock crashes, this customer knows that he can at least sell away his Alibaba stock at the price is fixed for the put-option thus minimizing his losses. However, in order to buy this contract, he needs to pay the bank a fee, and banks earn from this fee when they sell a put-option.

Now how does ELN come into the picture? When banks sell put-options, they have to put up capital as a margin to ensure that they are able to afford to buy back the underlying stock (Alibaba) of the put-option if the customer chooses to exercise the option. So instead of the bank putting up this capital, they are getting the customers who buy ELN to put up this capital ($100k in our example). So the bank does not need to fork out any capital, but still earns from the sale of the put-option. And with that sale, they use part of it to pay the coupons to the customers who purchased the ELN and they pocket the rest as pure profit.

Now if Alibaba price goes up, the customer who bought the put-option will not exercise his option, since his stock is now worth more and he does not need to sell it to the bank at the lower price promised in the option, and the option will expire. Bank will have earned from the put-option sale and sharing some of the profits with the customer who bought the ELN. But if Alibaba stock crashes, the customer who bought the put-option will exercise his option to sell his Alibaba stock to the bank at the agreed option price. So instead of the bank being forced to buy the stock from the customer, it transfer it to the customer who bought the ELN instead, who is forced to buy the Alibaba stock at the strike price. So at the end of the it, the bank walks away without having to own the badly performing Alibaba stock, which means the bank bears no risk at all, while the ELN customer bears all the risks.

I have simplified things quite a bit, but hopefully you can see that a customer who buys ELN basically is helping the bank make money for free. The bank bears almost no risk and they share any profits made with you. If things go well, everybody earns a little, but if things go bad, the ELN customer bears all the risk, while the bank walks away without any losses.

People considering buying ELN must understand that at the end of the day, they are trying to predict how the market will look for the stocks in the ELN. Nobody can accurately predict stock prices, not even Warren Buffet. And if you are confident enough of the stocks, then buy the stocks directly and own them instead of doing it through an ELN. Finally, you will also notice that most ELN bundles 1 or 2 stocks that are of higher volatility or risk. The reason being, the bank makes more money selling options on these high-risk stocks than on other more stable stocks. So they will usually need to bundle 1 or 2 of these stocks into the basket, which also means the ELN customer will be the one bearing the risk of these high-risk stocks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Recent Comments